The Search

Your Search Results

News from us

Newest Symbols

Newest Industries

Click to expand

Advertising

See Stocks

Automotive

See Stocks

E-Commerce

See Stocks

E-Learning

See Stocks

Electricity

See Stocks

Engineering

See Stocks

FlexShopper Inc.

Bullish

Bullish

Tattooed Chef Inc.

Neutral

Neutral

Hellofresh SE

Bullish

Bullish

Build-a-Bear Workshop Inc.

Outperform

Outperform

Stamps.com Inc.

Bullish

Bullish

Redfin Corporation

Bullish

Bullish

Perion Network Ltd.

Outperform

Outperform

Upwork Inc.

Bullish

Bullish

Chegg Inc.

Bullish

Bullish

Pinterest Inc.

Bullish

Bullish

Bluelinx Holdings Inc

Bullish

Bullish

Momentus Inc.

Neutral

Neutral

Mynaric AG

Neutral

Neutral

Virgin Galactic Holdings Inc.

Neutral

Neutral

Maxar Technologies Inc.

Neutral

Neutral

Sunrun Inc.

Bullish

Bullish

Steico SE

Neutral

Neutral

Alfen N.V.

Neutral

Neutral

Research

Content Cards

Swipe

Our Article

Weng Fine Art - Article

Research: The Monopoly of Balloon Sculptures Performed by the Emerging Arts Giant Weng Fine Art

In a world where investor and institutional flock to alternative asset classes to accommodate vast sums of money, printed relentlessly by central banks, the hunger for investable items is starvingly strong. This is the birthmother of cryptocurrencies, tokenized digital assets, or real-world scarce metals. But there is also an asset class dominated by names like da Vinci, Picasso, Koons or Hirst – the art market with its historic spawns. The biggest issue and dealbreaker is the required knowledge and capital needed to harvest return. Adding to that, the duopoly auctions houses Sotheby’s and Christie’s both were taken private in 2019 and 1999 – so the stock market lacks big art players. This gives the world’s largest public b2b arts dealer and the biggest public art ecommerce platform WENG FINE ART a monopoly.

Trend Radar –

Art market itself was dramatically disrupted by the pandemic with auctions sales falling 30% in 2020 (Arts Economics 2021) because of the suspension of live auctions and the shift to hybrid or full-on online auctions. This is the same trend that haunts traditional brick and mortar on the one side and boost ecommerce en contraire. Fat players were kicked out of the market and flexible teams were the clear winners in a dynamic year like 2020. What has to be outlined is that the mid-tier artwork market was not impacted as much as the main revenue drivers (+200m € trades) of the big auction houses.

Business model

Weng Fine Art (WFA) unites several sides of the art market: B2B trading, production and B2C ecommerce of limited editions, an auction database and the emerging fintech tokenization of artworks.

Historically Weng Fine Art started with its B2B dealership providing artwork sourcing for gallerists, auction houses and other arts dealers. This means the company is the bounding agent between the sales side and collectors in a mid-tier art environment. This is leveraged by the company’s balance sheet which can be much easier bolstered than the liquidity a small gallery has. The sourcing is supported by intense market analytics to harvest the greatest margins for every trade. But it is also its weakness because it is centered around knowledge and the company’s founder and CEO, which makes scalability rather hard. The small analyst team and upskilling is WFA’s key to success. Nevertheless, being the biggest player gives a certain negotiation edge and secures the juicy margins. A huge plus is that prices are driven by egomaniac participants (collectors), who do not a have the urge to ensure profits with their sales, and subjective opinions enable margins in heterogenic market environment. With a continuously improve balance sheet the price range of possibly traded artworks can reach up to the €1mio watermark. To sum this part of the business up, B2B trading is comparable to an art hedge fund or an actively managed artwork fund.

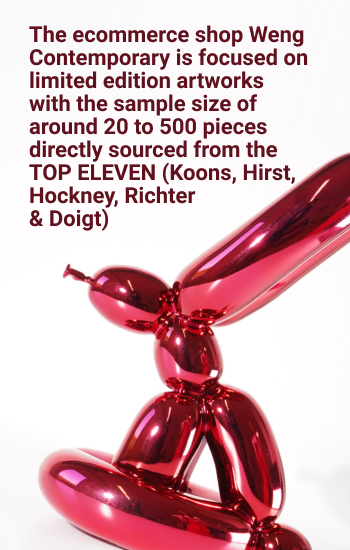

In 2014 the second pillar the ecommerce shop Weng Contemporary with its company ArtXX was founded. The online store is focused on limited edition artworks with the sample size of around 20 to 500 pieces sold through a concentrated sales team. Material is directly sourced from the artists like Damien Hirst, Ai WeiWei or Jeff Koons and continually price adjusted in its sale cycle. The targeted costumers differ form those that buy unique items, because the price range allows an entry point into the art market with the most famous artists. Once the original cycle is sold out Weng Contemporary engages as the secondary market for these addition to provide market liquidity.

Source: https://www.wengcontemporary.com/artworks/balloon-rabbit-red

An example for that is Jeff Koons Red Rabbit with was launched in 2017 for an initial price of almost 10000 $. After three price adjustments the 999 pieces were sold out after a year for the strike of close to 18000$. This started the secondary market offerings where prices hit the 25000$ mark in 2019. After handing out parts of Weng Fine Arts shares in ArtXX to early investors they still hold about 63% of the company. Growth catalysts are driven aquiring additional editions partnerships through their proven track record and an enhanced brand reach upscaling. The future for ArtXX is a public offering once it has grown large enough to guarantee liquid trading.

To further diversify WFA is involved in the public company Artnet. They have used the COVID crash to snack up to 21% of the company for low single digit prices which value has multiplied since then.

A newly founded business area will be focused on the fintech part of art through tokenization and tradability. Its goal is to make art investable and if plans with Artnet come to fruition its database might be a core feature for the pricing mechanism and information collection. The Ceo describes it as follows: “The future of the art market is not upheld by collectors or historians, but though the capital markets and retail investors”. The same development has been seen with gold. Once, gold was only jewelry for the nobility until in today’s times grams of gold are securitized and tradable with leverage on an instant.

Dividend policy

The company’s dividend policy is bound to the success of operations so in the last 5 years it has tripled with a low payout ratio. The 2020 payout yielded a 1+% return due to the share price movements. The track record also includes a phase when the dividend was only paid out to the free float holders because the biggest shareholder Weng renounce his right in these years to strengthen the company’s balance sheet.

Management

The CEO 67% of the shares with his chairman of the board in the second place (2%). This demonstrates how far aligned the management is with increasing shareholder value. Both have a background in steering the financial markets so using the given the tools is a core feature in their playbook.

The company’s strategies are transparently communicated and the CEO is always looking for the direct line to his shareholders through frequent FAQ sessions.

Competition & risks

The extremely fractionalized market allows the company to operate without direct competitors. The B2C parts has several local galleries that are serving an online presence, but they never have original editions, vast inventories (with prices) and the brand recognition like Weng Contemporary.

Privat companies startups like masterworks are trailblazing the artwork tokenization, but they operate on a closed base and are focused on the American market. This leaves space on a euro/asia area.

Valuation

A peerage comparison is not possible because arts participants are scare. Artnet is trading at almost 3 times sales but does not show growth or consistent profitability. Other ecommerce stocks do not post margins as ludicrous as Weng’s, so a runway success is imminent once they enter a different league.

Conclusion

The stock is an exotic portfolio addition that is driven by a determined financial artist. The unique opportunity to profit from elite frivolity combined with a reasonable valuated growth pipeline makes a great occasion for success.

Disclaimer & Conflict of interest

The author currently holds a position in the mentioned stock. The mentioned company does NOT compensate the author or the publisher of this website.

This post is not an investment advice and should not be treated as one. Please contact your local bank or broker for financial advice.

Weng Fine Art - Article

Research: The Monopoly of Balloon Sculptures Performed by the Emerging Arts Giant Weng Fine Art

In a world where investor and institutional flock to alternative asset classes to accommodate vast sums of money, printed relentlessly by central banks, the hunger for investable items is starvingly strong. This is the birthmother of cryptocurrencies, tokenized digital assets, or real-world scarce metals. But there is also an asset class dominated by names like da Vinci, Picasso, Koons or Hirst – the art market with its historic spawns. The biggest issue and dealbreaker is the required knowledge and capital needed to harvest return. Adding to that, the duopoly auctions houses Sotheby’s and Christie’s both were taken private in 2019 and 1999 – so the stock market lacks big art players. This gives the world’s largest public b2b arts dealer and the biggest public art ecommerce platform WENG FINE ART a monopoly.

Trend Radar -

Art market itself was dramatically disrupted by the pandemic with auctions sales falling 30% in 2020 (Arts Economics 2021) because of the suspension of live auctions and the shift to hybrid or full-on online auctions. This is the same trend that haunts traditional brick and mortar on the one side and boost ecommerce en contraire. Fat players were kicked out of the market and flexible teams were the clear winners in a dynamic year like 2020. What has to be outlined is that the mid-tier artwork market was not impacted as much as the main revenue drivers (+200m € trades) of the big auction houses.

Business model

Weng Fine Art (WFA) unites several sides of the art market: B2B trading, production and B2C ecommerce of limited editions, an auction database and the emerging fintech tokenization of artworks.

Historically Weng Fine Art started with its B2B dealership providing artwork sourcing for gallerists, auction houses and other arts dealers. This means the company is the bounding agent between the sales side and collectors in a mid-tier art environment. This is leveraged by the company’s balance sheet which can be much easier bolstered than the liquidity a small gallery has. The sourcing is supported by intense market analytics to harvest the greatest margins for every trade. But it is also its weakness because it is centered around knowledge and the company’s founder and CEO, which makes scalability rather hard. The small analyst team and upskilling is WFA's key to success. Nevertheless, being the biggest player gives a certain negotiation edge and secures the juicy margins. A huge plus is that prices are driven by egomaniac participants (collectors), who do not a have the urge to ensure profits with their sales, and subjective opinions enable margins in heterogenic market environment. With a continuously improve balance sheet the price range of possibly traded artworks can reach up to the €1mio watermark. To sum this part of the business up, B2B trading is comparable to an art hedge fund or an actively managed artwork fund.

In 2014 the second pillar the ecommerce shop Weng Contemporary with its company ArtXX was founded. The online store is focused on limited edition artworks with the sample size of around 20 to 500 pieces sold through a concentrated sales team. Material is directly sourced from the artists like Damien Hirst, Ai WeiWei or Jeff Koons and continually price adjusted in its sale cycle. The targeted costumers differ form those that buy unique items, because the price range allows an entry point into the art market with the most famous artists. Once the original cycle is sold out Weng Contemporary engages as the secondary market for these addition to provide market liquidity.

Source: https://www.wengcontemporary.com/artworks/balloon-rabbit-red

An example for that is Jeff Koons Red Rabbit with was launched in 2017 for an initial price of almost 10000 $. After three price adjustments the 999 pieces were sold out after a year for the strike of close to 18000$. This started the secondary market offerings where prices hit the 25000$ mark in 2019. After handing out parts of Weng Fine Arts shares in ArtXX to early investors they still hold about 63% of the company. Growth catalysts are driven aquiring additional editions partnerships through their proven track record and an enhanced brand reach upscaling. The future for ArtXX is a public offering once it has grown large enough to guarantee liquid trading.

To further diversify WFA is involved in the public company Artnet. They have used the COVID crash to snack up to 21% of the company for low single digit prices which value has multiplied since then.

A newly founded business area will be focused on the fintech part of art through tokenization and tradability. Its goal is to make art investable and if plans with Artnet come to fruition its database might be a core feature for the pricing mechanism and information collection. The Ceo describes it as follows: “The future of the art market is not upheld by collectors or historians, but though the capital markets and retail investors”. The same development has been seen with gold. Once, gold was only jewelry for the nobility until in today's times grams of gold are securitized and tradable with leverage on an instant.

Dividend policy

The company’s dividend policy is bound to the success of operations so in the last 5 years it has tripled with a low payout ratio. The 2020 payout yielded a 1+% return due to the share price movements. The track record also includes a phase when the dividend was only paid out to the free float holders because the biggest shareholder Weng renounce his right in these years to strengthen the company’s balance sheet.

Management

The CEO 67% of the shares with his chairman of the board in the second place (2%). This demonstrates how far aligned the management is with increasing shareholder value. Both have a background in steering the financial markets so using the given the tools is a core feature in their playbook.

The company’s strategies are transparently communicated and the CEO is always looking for the direct line to his shareholders through frequent FAQ sessions.

Competition & risks

The extremely fractionalized market allows the company to operate without direct competitors. The B2C parts has several local galleries that are serving an online presence, but they never have original editions, vast inventories (with prices) and the brand recognition like Weng Contemporary.

Privat companies startups like masterworks are trailblazing the artwork tokenization, but they operate on a closed base and are focused on the American market. This leaves space on a euro/asia area.

Valuation

A peerage comparison is not possible because arts participants are scare. Artnet is trading at almost 3 times sales but does not show growth or consistent profitability. Other ecommerce stocks do not post margins as ludicrous as Weng's, so a runway success is imminent once they enter a different league.

Conclusion

The stock is an exotic portfolio addition that is driven by a determined financial artist. The unique opportunity to profit from elite frivolity combined with a reasonable valuated growth pipeline makes a great occasion for success.

Disclaimer & Conflict of interest

The author currently holds a position in the mentioned stock. The mentioned company does NOT compensate the author or the publisher of this website.

This post is not an investment advice and should not be treated as one. Please contact your local bank or broker for financial advice.