Research: Pinterest - The Next Ad-Tech-Ecommerce Giant

Table of Content:

What sets PINS apart from their competitors?

Management

Business Model

Financial Highlights

Future Strategy and Outlook

Valuation

Conclusion

The company describes itself as a visual discovery engine for finding ideas like recipes, home, and style inspiration, and more. With their backwards ad products, they are the place where you find inspiration and then the product to fulfill your creative spark.

With Apple’s IOs 14 update and of widgetization of iPhone home screens, Pinterest boards were the first place to find inspiration. This example brought in millions of new users. The ongoing DIY (“Do it yourself”) / home improvement trend (while being on lockdown during the Covid-19 pandemic) is another trend that let the platforms usage surge.

Superior motive of providing positivity

They are a hub for hobbies and do not spread hate, controversial politics, and false body images like other social media platforms.

Speed

A behemoth like facebook has gotten too slow with fleshing out their planned shopping features. On the other hand, Pinterest (“PINS”) is young enough to launch new features and products ASAP.

Integrated shopping experience

The cooperation with Shopify (“Shopify offers ready to launch online shops systems and therefor related services for small to big businesses”) allows the retailer to directly upload their catalog to their Pinterest site.

Search as high intent service

Pinterest isn’t a platform that only rewards great photos. Pinterest is used for inspiration in the customers path to purchase something. They use Pinterest specifically to shop with also lets PINS crank up the ad density.

Target group with buying power

Pinterest reaches 83% of women ages 25-54. That same group makes 80% of the buying decisions in US households. But recent growth in millennial usage is also strong.

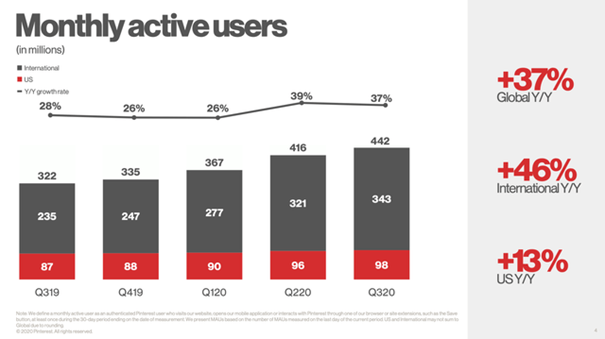

International story

Especially the last quarter showed a surge in international user paired with a better monetization of those.

Platform diversification strategy

CPG Marketers (“CPG = Consumer Packaged Goods”) intent to diverge from monopolists like Facebooks ad-platform, so Pinterest is the plaform for them. The facebook boycott has highlighted their opportunity.

Benjamin Silbermann is chariman of the board of directors, and the Co-Founder, President and Chief Executive Officer. Prior to co-founding Pinterest, Mr. Silbermann worked at Google from 2006 to 2008. He holds a Bachelor of Arts from Yale University.

Sharp has served as a Director of Pinterest since March 2019. Mr. Sharp is a Co-Founder of Pinterest and serves as their Chief Design & Creative Officer. Since joining Pinterest, he has overseen the creative, product and design teams. He was previously a product designer at Facebook from 2010 to 2011. Mr. Sharp studied Architecture at Columbia University and holds a Bachelor of Arts in History from the University of Chicago.

Pinterest uses a dual-class structure to concentrate voting power among major stakeholders including co-founders CEO Benjamin Silbermann (11,4%) and CCO Evan Sharp (2,1%). They own Class B shares.

Business Model

Pinterest has different ways to be used:

The home feed is where pins, people, topics, boards and brands that the algorithm chooses, are found.

Pins are bookmarks that people use to save ideas they love on Pinterest. Clicking through the pin, lets you visit the website to learn how to make it or where to buy it.

The saved pins are placed on your boards. Boards can be named and arranged on the profile.

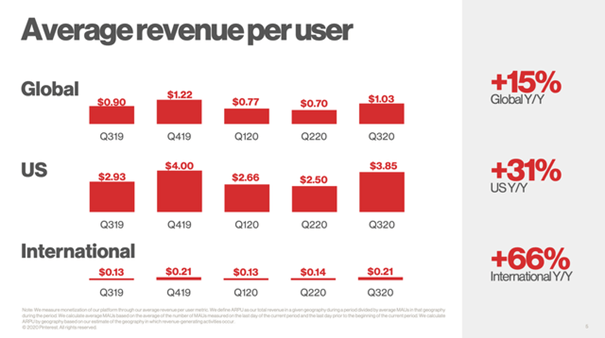

ARPU (“ARPU = Average Revenue Per User”) is notably going to tell $PINS forthcoming story. If US ARPU is gonna halfway meet facebooks US ARPU (40$) then those profits could 5-10x. But particularly the international ARPU shows great growth and even greater potential. Compared to facebooks international ARPU (Europe 12$, Asia 3,5$, Rest 2,2$) Pinterest totally lacks behind and has years of growth in front of them.

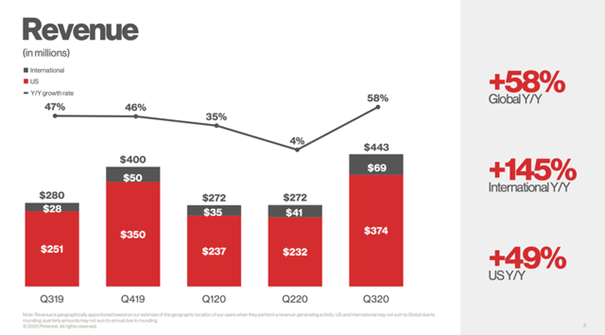

The cost metrics show the essence of growth companies. Every revenue extention allows to percentage wise reduce SG&A (“SG&A = Selling, General & Administrative Expense”) and will boost margins. Pinterest was able to channel its top-line strength in Q3 into profitability expansion.

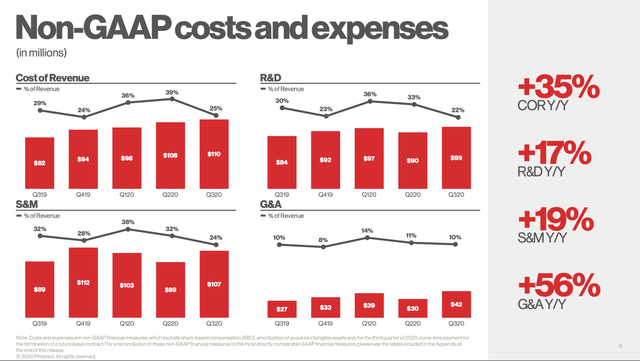

On the profitability side they are slowing closing the gap to the net margin breakeven. Particularly they have reach a new high with their adjusted EBITDA (“EBITDA = Earning Before Interest, Taxes, Deprecation & Amortization“) margin coming in at 21%. It will only grow from there. The net loss should not be a problem as long as growth is as strong as it is right now.

Future strategy und outlook

Further back-end works on autobidding and an overall process optimization should boost the ARPU in the coming quarters.

They are trying to improve the inventory of shoppable products and discoverability of those product. They are also building shopping surfaces, so you can take an inspirational image, and then see a catalog and inspiring inventory from Shopify or an other partner.

Pinterest has also invested heavily in maximizing the user experience by adding video content to their rooster. Especially this feature has seen massive success and it perfectly enhances the ad portfolio.

Those improvements work firmly together to increase user engagement. And strong user engagement will positivly lift advertiser demand. The vicious circle of great product design.

For now, Pinterest is still guiding for revenue to grow 60% year-over-year in Q4 2020, representing a slight further acceleration versus Q3 2020.

Moonshot

As outlined by Snap Inc’s (“Snap Inc. = Holding Company of Snapchat App”) AR (“AR = Augmented Reality”) growth story and Facebook R&D (“R&D = Research & Development”) focus, AR advertisement seems to be part of the future. So this is a development to watch, because Pinterest has to engage on this trend to future proof themselves. But also, this would be an fantastic addition to their lineup.

Covid Risks

The Covid Ad Market clearly favors online advertisment and is the accelerator in this trend. Further lockdowns solidify the stay at home improvement induced usage surge. So PINS is a winner in these times.

Valuation

On a PS-Ratio (“PS-Ratio = Price to Sales Ratio”) level Pinterest trades with an comparable valuation to snap eventhough their target group is better marketable and their “high intent service” should allow better margin ads. This is shown by PINS 40% wider gross profit margin.

One must argue that in an politically heated time Pinterest could be an ad safespace from censoring platforms like Facebook or Twitter. So approximately double the PS-ratio is warrented by a steeper top line growth.

The famous Rule of 40 is well surpassed with close to 60% top line growth and an EBITDA margin in the twenties.

Conclusion

The recent accelerating in top and bottom line growth reinforced by mentioned trends and the “online shift” megatrend provides a clear path to an even bigger company. So every shortterm setback gives a great entrypoint.

Disclaimer & Conflict of interest

The author currently holds a position in the mentioned stock and may sell his entire holding shortly after the release of this article. The mentioned company does NOT compensate the author or the publisher of this website.

This post is not an investment advice and should not be treated as one. Please contact your local bank or broker for financial advice.

Pinterest Inc. - Article

Research: Pinterest - The Next Ad-Tech-Ecommerce Giant

Table of Content:

What sets PINS apart from their competitors?

Management

Business Model

Financial Highlights

Future Strategy and Outlook

Valuation

Conclusion

The company describes itself as a visual discovery engine for finding ideas like recipes, home, and style inspiration, and more. With their backwards ad products, they are the place where you find inspiration and then the product to fulfill your creative spark.

With Apple's IOs 14 update and of widgetization of iPhone home screens, Pinterest boards were the first place to find inspiration. This example brought in millions of new users. The ongoing DIY ("Do it yourself") / home improvement trend (while being on lockdown during the Covid-19 pandemic) is another trend that let the platforms usage surge.

Superior motive of providing positivity

They are a hub for hobbies and do not spread hate, controversial politics, and false body images like other social media platforms.

Speed

A behemoth like facebook has gotten too slow with fleshing out their planned shopping features. On the other hand, Pinterest ("PINS") is young enough to launch new features and products ASAP.

Integrated shopping experience

The cooperation with Shopify ("Shopify offers ready to launch online shops systems and therefor related services for small to big businesses") allows the retailer to directly upload their catalog to their Pinterest site.

Search as high intent service

Pinterest isn’t a platform that only rewards great photos. Pinterest is used for inspiration in the customers path to purchase something. They use Pinterest specifically to shop with also lets PINS crank up the ad density.

Target group with buying power

Pinterest reaches 83% of women ages 25-54. That same group makes 80% of the buying decisions in US households. But recent growth in millennial usage is also strong.

International story

Especially the last quarter showed a surge in international user paired with a better monetization of those.

Platform diversification strategy

CPG Marketers ("CPG = Consumer Packaged Goods") intent to diverge from monopolists like Facebooks ad-platform, so Pinterest is the plaform for them. The facebook boycott has highlighted their opportunity.

Benjamin Silbermann is chariman of the board of directors, and the Co-Founder, President and Chief Executive Officer. Prior to co-founding Pinterest, Mr. Silbermann worked at Google from 2006 to 2008. He holds a Bachelor of Arts from Yale University.

Sharp has served as a Director of Pinterest since March 2019. Mr. Sharp is a Co-Founder of Pinterest and serves as their Chief Design & Creative Officer. Since joining Pinterest, he has overseen the creative, product and design teams. He was previously a product designer at Facebook from 2010 to 2011. Mr. Sharp studied Architecture at Columbia University and holds a Bachelor of Arts in History from the University of Chicago.

Pinterest uses a dual-class structure to concentrate voting power among major stakeholders including co-founders CEO Benjamin Silbermann (11,4%) and CCO Evan Sharp (2,1%). They own Class B shares.

Business Model

Pinterest has different ways to be used:

The home feed is where pins, people, topics, boards and brands that the algorithm chooses, are found.

Pins are bookmarks that people use to save ideas they love on Pinterest. Clicking through the pin, lets you visit the website to learn how to make it or where to buy it.

The saved pins are placed on your boards. Boards can be named and arranged on the profile.

ARPU ("ARPU = Average Revenue Per User") is notably going to tell $PINS forthcoming story. If US ARPU is gonna halfway meet facebooks US ARPU (40$) then those profits could 5-10x. But particularly the international ARPU shows great growth and even greater potential. Compared to facebooks international ARPU (Europe 12$, Asia 3,5$, Rest 2,2$) Pinterest totally lacks behind and has years of growth in front of them.

The cost metrics show the essence of growth companies. Every revenue extention allows to percentage wise reduce SG&A ("SG&A = Selling, General & Administrative Expense") and will boost margins. Pinterest was able to channel its top-line strength in Q3 into profitability expansion.

On the profitability side they are slowing closing the gap to the net margin breakeven. Particularly they have reach a new high with their adjusted EBITDA ("EBITDA = Earning Before Interest, Taxes, Deprecation & Amortization") margin coming in at 21%. It will only grow from there. The net loss should not be a problem as long as growth is as strong as it is right now.

Future strategy und outlook

Further back-end works on autobidding and an overall process optimization should boost the ARPU in the coming quarters.

They are trying to improve the inventory of shoppable products and discoverability of those product. They are also building shopping surfaces, so you can take an inspirational image, and then see a catalog and inspiring inventory from Shopify or an other partner.

Pinterest has also invested heavily in maximizing the user experience by adding video content to their rooster. Especially this feature has seen massive success and it perfectly enhances the ad portfolio.

Those improvements work firmly together to increase user engagement. And strong user engagement will positivly lift advertiser demand. The vicious circle of great product design.

For now, Pinterest is still guiding for revenue to grow 60% year-over-year in Q4 2020, representing a slight further acceleration versus Q3 2020.

Moonshot

As outlined by Snap Inc's ("Snap Inc. = Holding Company of Snapchat App") AR ("AR = Augmented Reality") growth story and Facebook R&D ("R&D = Research & Development") focus, AR advertisement seems to be part of the future. So this is a development to watch, because Pinterest has to engage on this trend to future proof themselves. But also, this would be an fantastic addition to their lineup.

Covid Risks

The Covid Ad Market clearly favors online advertisment and is the accelerator in this trend. Further lockdowns solidify the stay at home improvement induced usage surge. So PINS is a winner in these times.

Valuation

On a PS-Ratio ("PS-Ratio = Price to Sales Ratio") level Pinterest trades with an comparable valuation to snap eventhough their target group is better marketable and their "high intent service" should allow better margin ads. This is shown by PINS 40% wider gross profit margin.

One must argue that in an politically heated time Pinterest could be an ad safespace from censoring platforms like Facebook or Twitter. So approximately double the PS-ratio is warrented by a steeper top line growth.

The famous Rule of 40 is well surpassed with close to 60% top line growth and an EBITDA margin in the twenties.

Conclusion

The recent accelerating in top and bottom line growth reinforced by mentioned trends and the "online shift" megatrend provides a clear path to an even bigger company. So every shortterm setback gives a great entrypoint.

Disclaimer & Conflict of interest

The author currently holds a position in the mentioned stock and may sell his entire holding shortly after the release of this article. The mentioned company does NOT compensate the author or the publisher of this website.

This post is not an investment advice and should not be treated as one. Please contact your local bank or broker for financial advice.