The Search

Your Search Results

News from us

Newest Symbols

Newest Industries

Click to expand

Advertising

See Stocks

Automotive

See Stocks

E-Commerce

See Stocks

E-Learning

See Stocks

Electricity

See Stocks

Engineering

See Stocks

FlexShopper Inc.

Bullish

Bullish

Tattooed Chef Inc.

Neutral

Neutral

Hellofresh SE

Bullish

Bullish

Build-a-Bear Workshop Inc.

Outperform

Outperform

Stamps.com Inc.

Bullish

Bullish

Redfin Corporation

Bullish

Bullish

Perion Network Ltd.

Outperform

Outperform

Upwork Inc.

Bullish

Bullish

Chegg Inc.

Bullish

Bullish

Pinterest Inc.

Bullish

Bullish

Bluelinx Holdings Inc

Bullish

Bullish

Momentus Inc.

Neutral

Neutral

Mynaric AG

Neutral

Neutral

Virgin Galactic Holdings Inc.

Neutral

Neutral

Maxar Technologies Inc.

Neutral

Neutral

Sunrun Inc.

Bullish

Bullish

Steico SE

Neutral

Neutral

Alfen N.V.

Neutral

Neutral

Research

Content Cards

Swipe

Our Article

Lazydays Holdings Inc. - Article

Research Revamped: Lazydays RV - Recreational Vehicles Are Not as Lazy as You Might Think

Table of Content:

- Introduction to the Company

- Camping Trend

- Business Model & Financials

- Recent News and Updates

- Management & Share Structure

- Competition & Risks

- Valuation

- Conclusion

In a time when social distancing is the new normal, when borders are closed, and recreation is bound to one’s own home – people reconnect to nature. One way to explore the vast possibilities the United States´ national parks provide is by buying an RV and taking it on a road trip. The company that provides the wilderness seeker with the sale of new and used RVs, their servicing or even an RV resort is Lazydays Holdings, Inc. (NASDAQ: LAZY).

Camping Trend

RV market is experiencing unprecedented demand as consumers seek social distanced outdoor travel and leisure activities. RV’ing has the advantage of an Outdoor Lifestyle, it provides a safe and sanitary way of traveling, allows affordable vacation and the on-the-road lifestyle is spearheaded by socialmedia influencers( lovethatrv, rvlovetravel). More than 80M US households (growing by 2%) are active campers with the possibility to choose about 18000 camping sites around the country. The cliché RV-campers are retirees (growing by 10,000 new ones every day) but high growth rates for RVs are also seen with millennials. They are entering the market with earning period and have more disposable income. The majority of RV Buyers in 2020 made their first purchase. Those first-buyers typically look for a lower priced product(used or entrylevel new), because they tend to be a little younger.

RV production was hit dramatically by the pandemic, with many OEMs ( Original Equipment Manufacturer) completely shutting their facilties. This has caused prices on used and already produced vehicles to explode. On the demand side, many RV-lovers still wanted to buy their first vehicle, which allowed product margins to hit an all time high. OEM production levels continue to recover from the impact of the pandemic and production is continued to improve through the rest of 2021. RV inventory levels will begin to normalize sometime in mid-2021, so supply crunch is still in play for 2021.

In the near-term perspective, RV shipments increased 43% in November (2020), according to information from the RV Industry Association, but LAZY themselves have not reported on this month or the following.

Source: Lazy´s Investor Presentation+ Estimates: Baird forecast

Business and Financial Highlights

Their “Laydays” branded and for regional markets optimized dealerships operate in 8 states with an ever-growing footprint. At the beginning of 2021 the company operated 12 Dealerships and service centers. As the following map indicates – expansion into new markets provides a valuable growth opportunity.

Source: Lazy´s Investor Presentation

The revenue mix is dominated by the sale of new RVs (55%) followed by used RVs (33%). On the gross profit side the overweight of new RV sales diminishes into an equal weighted distribution throughout Lazy´s divisions.

Source: SEC Filing

For the new RVs division they work together with about 25 OEMs like Winnebago (WGO), Airstream or Thor Industries (NYSE:THO). This means they do not rely on only one manufacturer and can also profit from hypes around certain brands.

Used RV sales are supported by LAZY’s extensive trade-in policy and its wholesale purchase programs. They provide a attractive introductory chance for first-time buyers and easily start the services sales channel. Additionally, used RVs generate higher margins.

Financing & Insuring through LAZY’s partners helps to increase attachment rates and offers a complementary high‐margin .

The dealership’s parts & services add-on allows regional demand scaling to service the sold RVs and build a the LAZY brand to attract new customers.

Strategy

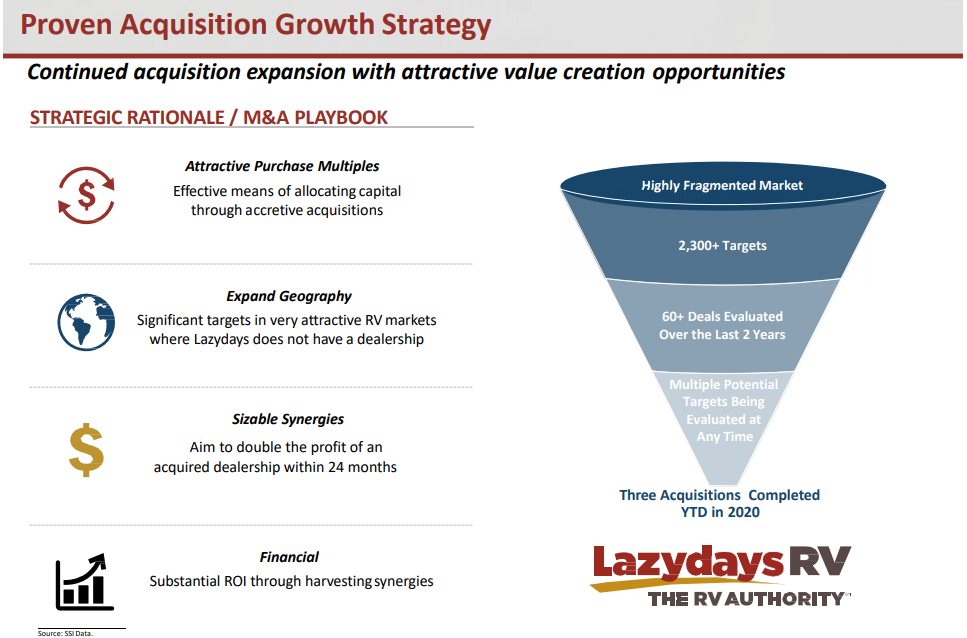

The company pursues an acquisition strategy by buying out mom and pop dealerships and streamlining their service and marketing efforts. The lastest acquisition was a family owned dealership in the larger Chicago area. Adding on to the near-term strategy they intent on diversifying the revenue by focusing on reoccurring sales through the servicing and parts sales division. Combined with the sale of used RVs in an attractive financing and insuring bundle, this strategic goal should boost the operating margins.

LAZY tries to manage their warchest very closely with the priority to deploying it to the investment with the highest returns. Currently, none of the many investment opportunities they have surveyed, including stock buybacks and buying back warrants come anywhere close to the returns they can get on new or acquired dealerships. They range muliples higher than single digit shareholder returns from debt/stock buybacks or dividends.

In the company’s Q3 earnings call they have announced to increase their expansion pipeline from 4 dealerships in 2020 to 8 in 2021. They continue to evaluate many actionable acquisition targets – assessing approximately 5 – 10 potential acquisitions at any given time and having looked at 60+ deals in the last 2 years. If the management’s plans are fully executed doubling LAZY’s footprint would be huge.

Source: Lazy´s Investor Presentation

E-Commerce Platform

The company’s physical sales channel is enforced by their vast selection of RVs found on their website. There you can also find maintenance tips and book service packages. They even let the buyer trade-in their old RV. Lazy makes it easy to directly calculate the monthly payment if the RV is going to be financed, which is one more lever to upsell the customer.

Every new dealership will benefit from access to their franchise.

Financials

LAZY perfectly capitalized on the special situation the pandemic provided. They have completely turned around their bottom-line and hit new records in Q3.

LAZY is now generating $6.5 million in EBITDA per month, has $82 million in cash and a $25 million in non-floor debt-plan. Total debt adds up to $180m, so with its recent surge in EBITDA a multiple of 2x can be reached. This allows them to easliy finance further acquisition if EBITDA is still growing.

Recent News and Updates

LAZYDAYS RV OPENS LAZYDAYS RV OF NASHVILLE: ITS 11TH FULL-SERVICE RV DEALERSHIP

Tampa, FL – Lazydays, The RV Authority®, announces that it has commenced sales and service operations at its new dealership in Murfreesboro, TN located just south of Nashville on I-24. The 42,000 square foot state-of-the-art facility becomes Lazydays 11th full-service RV dealership and it second dealership located in Tennessee. Lazydays RV of Nashville will carry Grand Design, Coachmen, Thor Motor Coach, Forest River, Tiffin and Winnebago brands.

“We are very excited to enter the rapidly growing Nashville market and expand our presence in Tennessee,” stated Ron Fleming, Lazydays’ Vice President and National General Manager. “We have built a beautiful facility designed to create a best-in-class experience for our customers. Our Nashville management team is very experienced, and we are confident they will achieve great success in this strong RV market.”

Lazydays now operates eleven dealerships in Florida, Colorado, Arizona, Minnesota, Tennessee, and Indiana; and operates a dedicated Service Center location near Houston, Texas.

-> The service expansion plan is going forward on strong feet

LAZYDAYS HOLDINGS, INC. COMPLETES ACQUISITION OF CAMP-LAND INC.

Tampa, FL – Yesterday, December 1st, Lazydays Holdings, Inc. (NASDAQCM: LAZY) (“Lazydays RV” or “Lazydays”) completed its acquisition of the assets of Camp-Land, Inc. (“Camp-Land RV”), located in Burns Harbor, Indiana. Camp-Land RV is a leading RV dealership serving the Chicagoland metro area and northern Indiana, with strong brands including Grand Design, Jayco, Coachmen, Thor Motorized and Winnebago. The acquisition further expands Lazydays footprint in the Midwest and allows for an expansion of brands offered at the recently acquired Lazydays RV of Elkhart.

“We are extremely pleased to complete this acquisition and execute on our geographic expansion strategy. The acquisition of Camp-Land RV not only gives Lazydays access to the Chicagoland market, but also allows us to add premier brands to our recently acquired Elkhart location,” stated William P. Murnane, Chairman and CEO of Lazydays. “I am pleased that Lazydays has been successful in accelerating our rate of geographic expansion. Camp-Land RV is our third completed acquisition over the last seven months, and will be followed shortly by the opening of our Nashville greenfield location in January 2021. In addition, we continue to work a strong pipeline of expansion opportunities that includes both acquisitions and greenfields.”

Lazydays now operates ten dealerships in Florida, Colorado, Arizona, Minnesota, Tennessee, and Indiana; and operates a dedicated Service Center location near Houston, Texas.

LAZYDAYS HOLDINGS, INC. REPORTS THIRD QUARTER 2020(ended September 30, 2020)FINANCIAL RESULTS

- Revenues for the third quarter of 2020 were $215.7 million; up $57.3 million, or 36.2%, versus 2019. Revenue from sales of Recreational Vehicles (“RVs”) was $194.6 million for the third quarter of 2020, up $55.7 million, or 40.1%, versus 2019. Unit sales excluding wholesale units, were 2,595 for the quarter, up 660 units, or 34.1% versus 2019. New and preowned RV sales revenues were $130.3 million and $64.2 million for the quarter, up 50.1% and 23.5% respectively compared to 2019.

- Gross profit for the quarter was $49.3 million; up $18.8 million, or 61.5%, versus 2019. Gross profit, excluding last-in-first-out (“LIFO”) adjustments, was $47.9 million, up $16.5 million, or 52.3%, versus 2019. Gross margin excluding LIFO adjustments increased between the two periods, to 22.2% in 2020 from 19.9% in 2019, with the change attributable to improved RV sales margins and mix of business. This gross profit comparison reflects a $2.3 million net difference in LIFO adjustments between the two periods.

- Selling, General and Administrative expense (“SG&A”) which excludes transaction costs, stock-based compensation, and depreciation and amortization, for the third quarter of 2020 was $28.6 million, up $3.0 million compared to the prior year. This increase is attributable to the additional overhead expenses associated with The Villages dealership acquired in August 2019, the service center near Houston that started up operations in mid-February 2020, the Phoenix dealership acquired in May 2020 and increased performance wages driven by the higher unit sales and revenue, partially offset by overhead cost reduction actions taken in April 2020.

- Adjusted EBITDA, a non-GAAP financial measure, was $19.0 million for the third quarter of 2020, up $13.7 million compared to 2019. This is another record high quarterly Adjusted EBITDA for Lazydays, beating the recently set previous record of $14.9 million in the second quarter of 2020.

- Net income for the third quarter of 2020 was $11.6 million, or 55¢ per share, as compared to net loss of $2.5 million, or 41¢ per share, in 2019. This $14.1 million net improvement was primarily the result of incremental profits driven by the growth in sales, the reduced amortization of stock based compensation, as well as a $0.6 million decrease in interest expense.

- As of September 30, 2020, cash was $81.7 million, up $50.2 million from December 31, 2019.

- Year over year demand and margins in October 2020 continued to be to be strong, and manufacturers are shipping product to us at levels that are slightly ahead of retail sales.

Management & Share Structure

CEO: William Murnane has served as Chairman of the board of Lazydays since 2009. He joined the company as Chief Executive officer in December 2016. From 2008 through 2016, Mr. Murnane, was a former principal and operating partner at Wayzata Investment Partners LLC, where he specialized in operational turn-arounds. From 2000 to 2007, Mr. Murnane was Chairman and Chief Executive Officer of Innovex, Inc., an international manufacturer of components used in high technology electronics. Mr. Murnane started his career with United Parcel Service when he held various engineering and management positions. Mr. Murnane holds a BS in Engineering from New Jersey Institute of Technology, an MS in Operations Research from the University of Maryland, and an MBA from the Harvard Business School.

”And we’re not looking for a 1 month or a 3-month or a 6-month results from that. We’re patient. We’re in this for the long haul.”

The CEO specifically stands out, because of comments like this that show his long-term focus.

Insiders and Institutions to watch:

Competition & Risks

Camping World (CWH)

CWH is a direct competitor. Their market cap is 14x higher, revenue is 7x higher and their Q3 net income was 13x higher than LAZY’s. They engage, next to their dealership business, also on the retail of RV accessories and supplies. A big red flag is the huge dividend hike, the special dividend and the buyback program their management has announced. It shows CWH’s returns for acquisitions are to low to justify them and demonstrates that company is not on a growth track like LAZY anymore

The market of around 500k new RVs sold every year is big enough for lots of regional players, so they are not a huge risk. But they could potentially buy LAZY.

Startups

The peer-to-peer segment is growing incredibly fast with stand-alone companies such as Outdoorsy, which have very high valuations.(Estimates reach up to $500m; last founding round Jan 2019) They engage in the rental p2p business of RVs. But they are still private and the rental business itself is very hard with low returns.

OEMs

Public companies like Winnebago (WGO) or Thor Industries (NYSE:THO) have different business model, but they benefit in the same way as LAZY from the RV-trend. The problem is they cannot grow their operations beyond the demand side. LAZY offers the better deal for investors because they can easily build or acquire further locations. Adding to that issue is that rivalry between OEMs is a lot more fierce than the competition a all-brands dealership has.

Risks

On the risk side, there is always the possibility for the OEMs to undercut the traditional dealership structure by directly selling to the customer. (Tesla is the best example for that) But this does not seems like a huge risk.

Selling RVs is a cyclical business and in an economic downturn shares will be hit hard. This is one reason why lower multiples have to be taken to account.

Valuation

Recent developments shown by the Q3 results indicate an overall still strong demand. The table below demonstrates valuation discrepancies within LAZY’S peergroup:

This table simply manifests OEMs are in comparison to their RVs’ dealer way to expensive in their top and bottom-line valuation. Even CWH cannot keep up with LAZY’s growth, valuation and business strategy as mentioned before.

Conclusion

RVs provide a great leisure investment opportunity with in general low valuations, with profits and growth. You could call it the best of all worlds with LAZY as the best choice in this industry. Other tourism investment (airlines, hotels or cruiseships) will need years to reach this point if they survive that far. As its valuation and perspective indicates – LAZY is a clear buy!

General Warning

Due to the small marketcap and the low float (the amount of shares circling around and traded, which are not held by major investors) of LAZY shares, there are certain risks and an increased volatility.

Disclaimer & Conflict of interest

The author currently holds a position in the mentioned stock and may sell his entire holding shortly after the release of this article. The mentioned company does NOT compensate the author or the publisher of this website.

This post is not an investment advice and should not be treated as one. Please contact your local bank or broker for financial advice.

Lazydays Holdings Inc. - Article

Research Revamped: Lazydays RV - Recreational Vehicles Are Not as Lazy as You Might Think

Table of Content:

- Introduction to the Company

- Camping Trend

- Business Model & Financials

- Recent News and Updates

- Management & Share Structure

- Competition & Risks

- Valuation

- Conclusion

In a time when social distancing is the new normal, when borders are closed, and recreation is bound to one’s own home - people reconnect to nature. One way to explore the vast possibilities the United States´ national parks provide is by buying an RV and taking it on a road trip. The company that provides the wilderness seeker with the sale of new and used RVs, their servicing or even an RV resort is Lazydays Holdings, Inc. (NASDAQ: LAZY).

Camping Trend

RV market is experiencing unprecedented demand as consumers seek social distanced outdoor travel and leisure activities. RV’ing has the advantage of an Outdoor Lifestyle, it provides a safe and sanitary way of traveling, allows affordable vacation and the on-the-road lifestyle is spearheaded by socialmedia influencers( lovethatrv, rvlovetravel). More than 80M US households (growing by 2%) are active campers with the possibility to choose about 18000 camping sites around the country. The cliché RV-campers are retirees (growing by 10,000 new ones every day) but high growth rates for RVs are also seen with millennials. They are entering the market with earning period and have more disposable income. The majority of RV Buyers in 2020 made their first purchase. Those first-buyers typically look for a lower priced product(used or entrylevel new), because they tend to be a little younger.

RV production was hit dramatically by the pandemic, with many OEMs ( Original Equipment Manufacturer) completely shutting their facilties. This has caused prices on used and already produced vehicles to explode. On the demand side, many RV-lovers still wanted to buy their first vehicle, which allowed product margins to hit an all time high. OEM production levels continue to recover from the impact of the pandemic and production is continued to improve through the rest of 2021. RV inventory levels will begin to normalize sometime in mid-2021, so supply crunch is still in play for 2021.

In the near-term perspective, RV shipments increased 43% in November (2020), according to information from the RV Industry Association, but LAZY themselves have not reported on this month or the following.

Source: Lazy´s Investor Presentation+ Estimates: Baird forecast

Business and Financial Highlights

Their “Laydays” branded and for regional markets optimized dealerships operate in 8 states with an ever-growing footprint. At the beginning of 2021 the company operated 12 Dealerships and service centers. As the following map indicates – expansion into new markets provides a valuable growth opportunity.

Source: Lazy´s Investor Presentation

The revenue mix is dominated by the sale of new RVs (55%) followed by used RVs (33%). On the gross profit side the overweight of new RV sales diminishes into an equal weighted distribution throughout Lazy´s divisions.

Source: SEC Filing

For the new RVs division they work together with about 25 OEMs like Winnebago (WGO), Airstream or Thor Industries (NYSE:THO). This means they do not rely on only one manufacturer and can also profit from hypes around certain brands.

Used RV sales are supported by LAZY’s extensive trade-in policy and its wholesale purchase programs. They provide a attractive introductory chance for first-time buyers and easily start the services sales channel. Additionally, used RVs generate higher margins.

Financing & Insuring through LAZY’s partners helps to increase attachment rates and offers a complementary high‐margin .

The dealership’s parts & services add-on allows regional demand scaling to service the sold RVs and build a the LAZY brand to attract new customers.

Strategy

The company pursues an acquisition strategy by buying out mom and pop dealerships and streamlining their service and marketing efforts. The lastest acquisition was a family owned dealership in the larger Chicago area. Adding on to the near-term strategy they intent on diversifying the revenue by focusing on reoccurring sales through the servicing and parts sales division. Combined with the sale of used RVs in an attractive financing and insuring bundle, this strategic goal should boost the operating margins.

LAZY tries to manage their warchest very closely with the priority to deploying it to the investment with the highest returns. Currently, none of the many investment opportunities they have surveyed, including stock buybacks and buying back warrants come anywhere close to the returns they can get on new or acquired dealerships. They range muliples higher than single digit shareholder returns from debt/stock buybacks or dividends.

In the company's Q3 earnings call they have announced to increase their expansion pipeline from 4 dealerships in 2020 to 8 in 2021. They continue to evaluate many actionable acquisition targets – assessing approximately 5 – 10 potential acquisitions at any given time and having looked at 60+ deals in the last 2 years. If the management's plans are fully executed doubling LAZY's footprint would be huge.

Source: Lazy´s Investor Presentation

E-Commerce Platform

The company’s physical sales channel is enforced by their vast selection of RVs found on their website. There you can also find maintenance tips and book service packages. They even let the buyer trade-in their old RV. Lazy makes it easy to directly calculate the monthly payment if the RV is going to be financed, which is one more lever to upsell the customer.

Every new dealership will benefit from access to their franchise.

Financials

LAZY perfectly capitalized on the special situation the pandemic provided. They have completely turned around their bottom-line and hit new records in Q3.

LAZY is now generating $6.5 million in EBITDA per month, has $82 million in cash and a $25 million in non-floor debt-plan. Total debt adds up to $180m, so with its recent surge in EBITDA a multiple of 2x can be reached. This allows them to easliy finance further acquisition if EBITDA is still growing.

Recent News and Updates

LAZYDAYS RV OPENS LAZYDAYS RV OF NASHVILLE: ITS 11TH FULL-SERVICE RV DEALERSHIP

Tampa, FL – Lazydays, The RV Authority®, announces that it has commenced sales and service operations at its new dealership in Murfreesboro, TN located just south of Nashville on I-24. The 42,000 square foot state-of-the-art facility becomes Lazydays 11th full-service RV dealership and it second dealership located in Tennessee. Lazydays RV of Nashville will carry Grand Design, Coachmen, Thor Motor Coach, Forest River, Tiffin and Winnebago brands.

“We are very excited to enter the rapidly growing Nashville market and expand our presence in Tennessee,” stated Ron Fleming, Lazydays’ Vice President and National General Manager. “We have built a beautiful facility designed to create a best-in-class experience for our customers. Our Nashville management team is very experienced, and we are confident they will achieve great success in this strong RV market.”

Lazydays now operates eleven dealerships in Florida, Colorado, Arizona, Minnesota, Tennessee, and Indiana; and operates a dedicated Service Center location near Houston, Texas.

-> The service expansion plan is going forward on strong feet

LAZYDAYS HOLDINGS, INC. COMPLETES ACQUISITION OF CAMP-LAND INC.

Tampa, FL – Yesterday, December 1st, Lazydays Holdings, Inc. (NASDAQCM: LAZY) (“Lazydays RV” or “Lazydays”) completed its acquisition of the assets of Camp-Land, Inc. (“Camp-Land RV”), located in Burns Harbor, Indiana. Camp-Land RV is a leading RV dealership serving the Chicagoland metro area and northern Indiana, with strong brands including Grand Design, Jayco, Coachmen, Thor Motorized and Winnebago. The acquisition further expands Lazydays footprint in the Midwest and allows for an expansion of brands offered at the recently acquired Lazydays RV of Elkhart.

“We are extremely pleased to complete this acquisition and execute on our geographic expansion strategy. The acquisition of Camp-Land RV not only gives Lazydays access to the Chicagoland market, but also allows us to add premier brands to our recently acquired Elkhart location,” stated William P. Murnane, Chairman and CEO of Lazydays. “I am pleased that Lazydays has been successful in accelerating our rate of geographic expansion. Camp-Land RV is our third completed acquisition over the last seven months, and will be followed shortly by the opening of our Nashville greenfield location in January 2021. In addition, we continue to work a strong pipeline of expansion opportunities that includes both acquisitions and greenfields.”

Lazydays now operates ten dealerships in Florida, Colorado, Arizona, Minnesota, Tennessee, and Indiana; and operates a dedicated Service Center location near Houston, Texas.

LAZYDAYS HOLDINGS, INC. REPORTS THIRD QUARTER 2020(ended September 30, 2020)FINANCIAL RESULTS

- Revenues for the third quarter of 2020 were $215.7 million; up $57.3 million, or 36.2%, versus 2019. Revenue from sales of Recreational Vehicles ("RVs") was $194.6 million for the third quarter of 2020, up $55.7 million, or 40.1%, versus 2019. Unit sales excluding wholesale units, were 2,595 for the quarter, up 660 units, or 34.1% versus 2019. New and preowned RV sales revenues were $130.3 million and $64.2 million for the quarter, up 50.1% and 23.5% respectively compared to 2019.

- Gross profit for the quarter was $49.3 million; up $18.8 million, or 61.5%, versus 2019. Gross profit, excluding last-in-first-out (“LIFO”) adjustments, was $47.9 million, up $16.5 million, or 52.3%, versus 2019. Gross margin excluding LIFO adjustments increased between the two periods, to 22.2% in 2020 from 19.9% in 2019, with the change attributable to improved RV sales margins and mix of business. This gross profit comparison reflects a $2.3 million net difference in LIFO adjustments between the two periods.

- Selling, General and Administrative expense (“SG&A”) which excludes transaction costs, stock-based compensation, and depreciation and amortization, for the third quarter of 2020 was $28.6 million, up $3.0 million compared to the prior year. This increase is attributable to the additional overhead expenses associated with The Villages dealership acquired in August 2019, the service center near Houston that started up operations in mid-February 2020, the Phoenix dealership acquired in May 2020 and increased performance wages driven by the higher unit sales and revenue, partially offset by overhead cost reduction actions taken in April 2020.

- Adjusted EBITDA, a non-GAAP financial measure, was $19.0 million for the third quarter of 2020, up $13.7 million compared to 2019. This is another record high quarterly Adjusted EBITDA for Lazydays, beating the recently set previous record of $14.9 million in the second quarter of 2020.

- Net income for the third quarter of 2020 was $11.6 million, or 55¢ per share, as compared to net loss of $2.5 million, or 41¢ per share, in 2019. This $14.1 million net improvement was primarily the result of incremental profits driven by the growth in sales, the reduced amortization of stock based compensation, as well as a $0.6 million decrease in interest expense.

- As of September 30, 2020, cash was $81.7 million, up $50.2 million from December 31, 2019.

- Year over year demand and margins in October 2020 continued to be to be strong, and manufacturers are shipping product to us at levels that are slightly ahead of retail sales.

Management & Share Structure

CEO: William Murnane has served as Chairman of the board of Lazydays since 2009. He joined the company as Chief Executive officer in December 2016. From 2008 through 2016, Mr. Murnane, was a former principal and operating partner at Wayzata Investment Partners LLC, where he specialized in operational turn-arounds. From 2000 to 2007, Mr. Murnane was Chairman and Chief Executive Officer of Innovex, Inc., an international manufacturer of components used in high technology electronics. Mr. Murnane started his career with United Parcel Service when he held various engineering and management positions. Mr. Murnane holds a BS in Engineering from New Jersey Institute of Technology, an MS in Operations Research from the University of Maryland, and an MBA from the Harvard Business School.

”And we're not looking for a 1 month or a 3-month or a 6-month results from that. We're patient. We're in this for the long haul.”

The CEO specifically stands out, because of comments like this that show his long-term focus.

Insiders and Institutions to watch:

Competition & Risks

Camping World (CWH)

CWH is a direct competitor. Their market cap is 14x higher, revenue is 7x higher and their Q3 net income was 13x higher than LAZY's. They engage, next to their dealership business, also on the retail of RV accessories and supplies. A big red flag is the huge dividend hike, the special dividend and the buyback program their management has announced. It shows CWH's returns for acquisitions are to low to justify them and demonstrates that company is not on a growth track like LAZY anymore

The market of around 500k new RVs sold every year is big enough for lots of regional players, so they are not a huge risk. But they could potentially buy LAZY.

Startups

The peer-to-peer segment is growing incredibly fast with stand-alone companies such as Outdoorsy, which have very high valuations.(Estimates reach up to $500m; last founding round Jan 2019) They engage in the rental p2p business of RVs. But they are still private and the rental business itself is very hard with low returns.

OEMs

Public companies like Winnebago (WGO) or Thor Industries (NYSE:THO) have different business model, but they benefit in the same way as LAZY from the RV-trend. The problem is they cannot grow their operations beyond the demand side. LAZY offers the better deal for investors because they can easily build or acquire further locations. Adding to that issue is that rivalry between OEMs is a lot more fierce than the competition a all-brands dealership has.

Risks

On the risk side, there is always the possibility for the OEMs to undercut the traditional dealership structure by directly selling to the customer. (Tesla is the best example for that) But this does not seems like a huge risk.

Selling RVs is a cyclical business and in an economic downturn shares will be hit hard. This is one reason why lower multiples have to be taken to account.

Valuation

Recent developments shown by the Q3 results indicate an overall still strong demand. The table below demonstrates valuation discrepancies within LAZY'S peergroup:

This table simply manifests OEMs are in comparison to their RVs' dealer way to expensive in their top and bottom-line valuation. Even CWH cannot keep up with LAZY's growth, valuation and business strategy as mentioned before.

Conclusion

RVs provide a great leisure investment opportunity with in general low valuations, with profits and growth. You could call it the best of all worlds with LAZY as the best choice in this industry. Other tourism investment (airlines, hotels or cruiseships) will need years to reach this point if they survive that far. As its valuation and perspective indicates - LAZY is a clear buy!

General Warning

Due to the small marketcap and the low float (the amount of shares circling around and traded, which are not held by major investors) of LAZY shares, there are certain risks and an increased volatility.

Disclaimer & Conflict of interest

The author currently holds a position in the mentioned stock and may sell his entire holding shortly after the release of this article. The mentioned company does NOT compensate the author or the publisher of this website.

This post is not an investment advice and should not be treated as one. Please contact your local bank or broker for financial advice.